Dear maria,

Right now, IMF Western Hemisphere Department Director Alejandro Werner is holding a live virtual press conference on the latest economic outlook for Latin America and the Caribbean. You can also read his newest blog below in full. Translations coming soon.

Latin America and the Caribbean have become the new COVID-19 global epicenter. The human cost has been tragic, with over 100,000 lives lost. The economic toll has also been steep. The World Economic Outlook Update now estimates the region to shrink by 9.4 percent in 2020, four percentage points worse than the April projection and the worst recession on record. A mild recovery to +3.7 percent is projected in 2021.

The pandemic

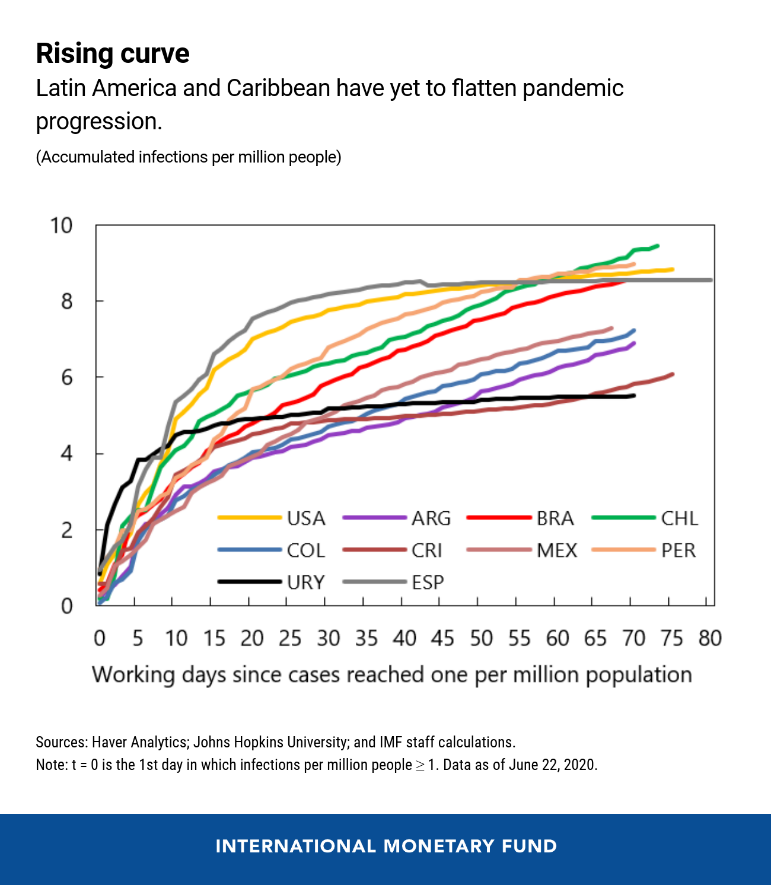

The rates of COVID-19 infections and deaths per capita are approaching those in Europe and the United States, with the total number of cases accounting for about 25 percent of the worldwide total.

Against this backdrop, countries should be very cautious when considering reopening their economies and allow science and data to guide the process. Indeed, many countries in the region have high levels of informality and low preparedness to handle new outbreaks, like a high occupancy of intensive care unit beds and low testing and tracing capacity.

Recent economic developments

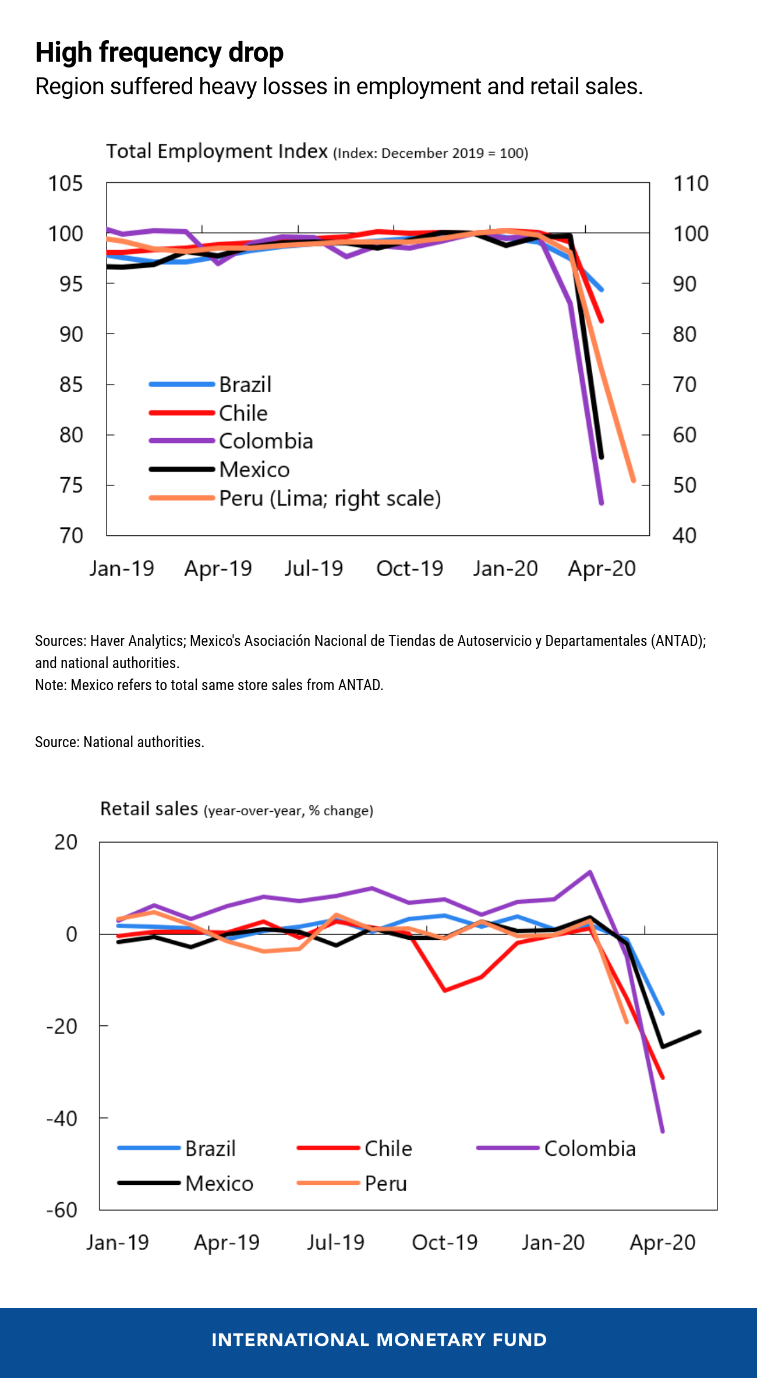

Weaker economic data and more protracted COVID-19 outbreaks explain the significant downward revisions compared to our April forecasts. First quarter growth was worse than expected for most countries, while high frequency indicators – like industrial production, electricity consumption, retail sales, and employment – suggest that the decline in the second quarter will be deeper than projected in April. The pandemic’s still rapid spread indicates that social distancing measures will need to remain in place for a longer time, depressing economic activity in the second half of 2020 and leaving more scarring going forward.

Despite the difficult outlook, external financial conditions have eased in recent weeks, largely reflecting strong actions by advanced economies’ central banks, which have allowed some countries to issue debt abroad. However, financial conditions are still tighter than before the pandemic and are expected to remain volatile going forward.

Risks remain elevated. The pandemic could worsen and last longer, depressing economic activity, stressing corporate balance sheets, raising poverty and inequality, and rekindling social tensions across the region. Upside surprises could also happen. Some recent high frequency indicators for advanced economies have been better than expected. Global growth could be stronger than expected, supporting exports, commodity prices, and tourism.

Policy priorities

The immediate priority for fiscal policy is to continue protecting lives and livelihoods, which given the limited fiscal space in the region, will require reprioritizing expenditure and increasing its efficiency. Policymakers will need to find creative ways to reach different segments of society, especially where informality is high. The fallout from the pandemic and associated policy response will also raise medium-term debt sustainability concerns in several countries. Commitment to a medium-term plan of fiscal consolidation and growth-enhancing structural reforms will be key to mitigate these concerns.

Monetary policy should remain accommodative given the subdued inflation outlook, negative output gaps, and elevated unemployment. Additional policy rate cuts and measures targeted to specific markets should be considered where necessary and possible, to support economic activity and ensure proper functioning of financial markets.

Measures to maintain employment relationships, such as payroll support and financing of working capital will be important to avoid the closure of otherwise viable businesses, reduce long-term unemployment, support the recovery, minimize scarring and increase potential growth. Containment and mitigation policies should be appropriately calibrated to avoid a second pandemic wave and manage localized outbreaks.

In Argentina, GDP is expected to decline by about 10 percent in 2020, with heightened risks. Growth was revised down as the longer quarantine in the Buenos Aires metropolitan area, a sharply weaker external demand and worse commodity prices should more than offset the fiscal support package, which remains constrained by limited financing options. Uncertainties related to the debt restructuring process continue to weigh on confidence.

Brazil’s, real GDP is projected to fall by 9 percent in 2020 amid high uncertainty, followed by a rebound of 3.6 percent in 2021. The authorities have responded strongly to the pandemic with decisive interest rate cuts, and significant fiscal and liquidity packages, including direct cash transfers targeted to vulnerable groups. The withdrawal of this stimulus however will weigh on growth in 2021 amid a domestic economy that was still shrugging off the 2015/16 recession. In this context, accommodative monetary policy will be essential to support the cyclical recovery while resuming the government’s fiscal and structural reform agenda is key to preserving fiscal sustainability and boosting potential growth and investor confidence.

In Chile, real GDP is projected to decline by 7.5 percent in 2020 and rebound by 5.0 percent in 2021. Following a resilient performance in the first quarter, economic activity is expected to contract sharply in the second quarter owing to the strict social distancing measures, and to a lesser extent, weaker external demand from trading partners. A rebound in activity is expected to start in the third quarter and continue into 2021, supported by unprecedented fiscal, monetary and financial sector measures.

Colombia took early actions to limit the spread of the virus, but economic disruptions associated with the pandemic (including lower oil prices) are expected to generate the first recession in two decades. Following a weak first quarter, GDP is expected to contract by 7.8 percent in 2020, but growth should rebound to 4.0 percent in 2021 as the health situation stabilizes at home and elsewhere. In response, the central bank has cut policy rates and supported market liquidity, while the fiscal rule was suspended for two years to provide sufficient flexibility to respond to the health and economic crises.

The outbreak fallout for Mexico is compounded by the fall in oil prices, international financial markets volatility, disruptions to global value chains, and weakening business confidence as also reflected in declining investment pre-Covid. Real GDP is expected to fall by 10.5 percent in 2020 with growth in 2021 expected to recover a modest portion of the lost output. Monetary policy is expected to loosen further to accommodate the demand shock element of the crisis and preserve the functioning of financial markets. However, the fiscal response is the smallest among G20 countries, risking a deeper contraction and slower recovery with significant economic scarring. Mexico should ramp up spending now to protect lives and livelihoods and craft a credible medium-term fiscal reform that provides more short-term policy space and close fiscal gaps.

In Peru, the growth projection for 2020 has been revised down markedly to -14 percent, as weaker external demand and a longer than expected lockdown period have so far more than offset the government’s significant economic support and translated into large employment losses. With the lockdown restrictions lifted in the second semester, economic activity is expected to gradually recover, reaching a 6½ percent expansion in 2021. Downside risks remain prominent, however, and are particularly linked to domestic and global challenges in bringing the Covid-19 pandemic under control.

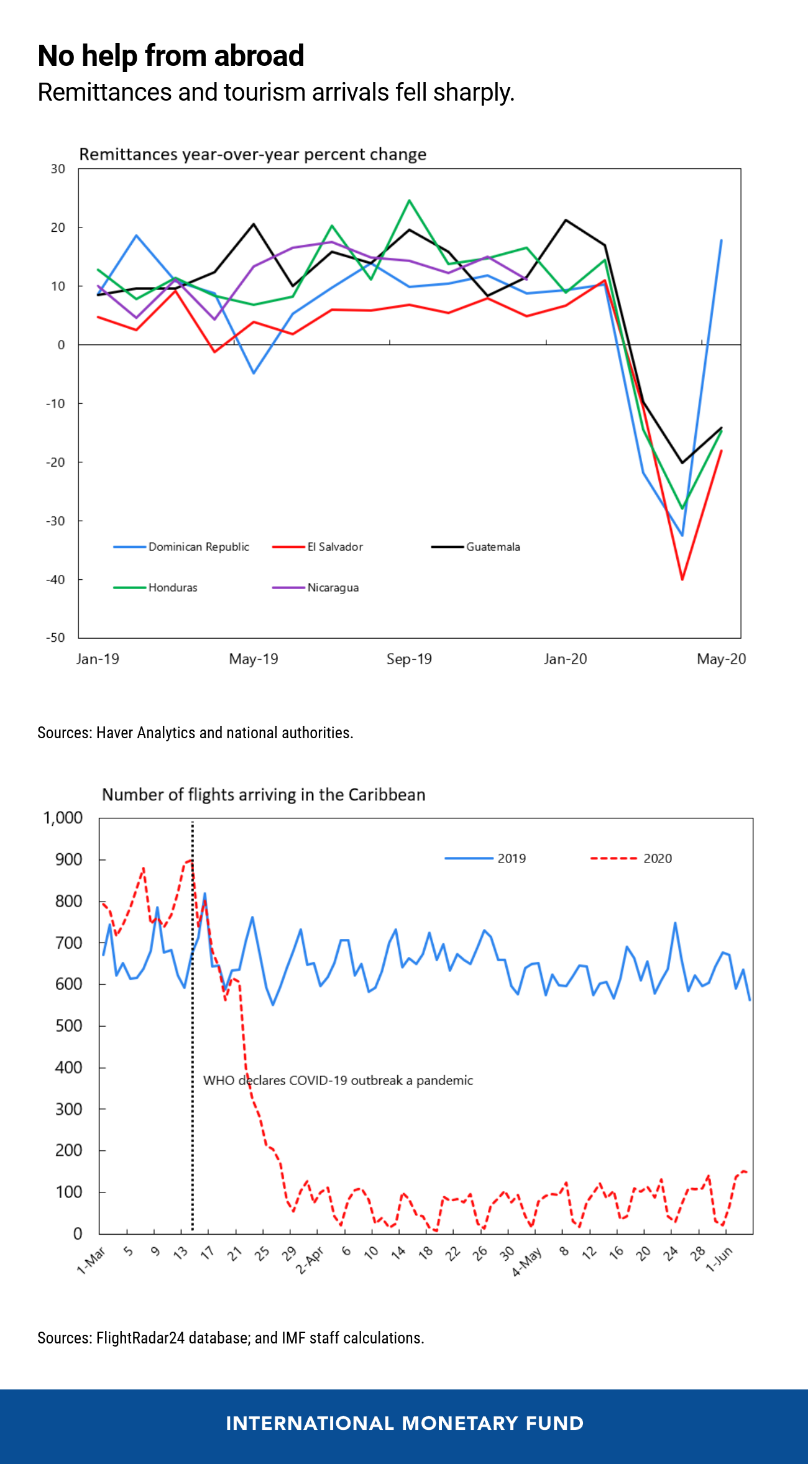

Central America, Panama, and the Dominican Republic (CAPDR) will experience a deep recession in 2020 and a gradual recovery starting in 2021. Growth is being affected by domestic lockdowns and global spillovers through trade, tourism, and remittances. The contraction in trade will have a particularly strong impact in Panama, El Salvador and Nicaragua, the collapse in tourism in the Dominican Republic and Costa Rica, and weaker remittances in the Northern Triangle and Nicaragua. Idiosyncratic factors are also at play, notably natural disasters in El Salvador. A palliative is that falling oil prices are improving the terms of trade.

Countries in CAPDR have mitigated the pandemic by increasing health and social spending for unemployed and vulnerable households. Where feasible, monetary policy easing and credit guarantees are supporting financing for business, and tax deferrals and specific sectoral support through the budget are aiming at relaxing liquidity constraints in some countries.

The Caribbean economies have managed to flatten the COVID-19 curve, but their key lifelines have collapsed. With tourism coming to a virtual standstill and key source markets in advanced economies plunging into deeper recession, the region is likely to experience a very sharp and protracted contraction in economic activity. Despite the reopening of borders starting in June for some Caribbean countries, international tourist arrivals are expected to return to pre-crisis levels only gradually over the next three years. In addition, the steep drop in oil prices is hurting commodity exporters through a loss in exports and fiscal revenues. The ongoing hurricane season poses additional risks.

The IMF’s support

The Fund has acted swiftly to support its membership with quick and significant injections of emergency financing. Of the 70 loans approved since the pandemic began, totaling US$ 25 billion, 17 were for countries in the region, for a total of US$ 5.2 billion. Additionally, access to the Flexible Credit Line was approved for Chile and Peru and renewed for Colombia. Together with Mexico, the total backstop provided to the region through the Flexible Credit Line amounts to US$ 107 billion.

We stand ready to use the IMF’s financial clout, policy advice and capacity development resources to help Latin America and the Caribbean achieve a stronger recovery.

*****

Take good care,

|